There is a very common term used in the financial world called house poor. The exact meaning of the term can be found at the link below but in layman’s terms … it means you’re living a life style beyond what your earnings can pay for. While we say house poor, it can also be car poor, utility poor or lifestyle poor. A combination of more than one of these and you have some issues for sure.

So the question is how do we end up there? Not many people are going to intentionally put themselves in debt to such an extent that they cant get by. The most common way is our ego gets in the way. You see a friend with a nice new car so we have to have one. Or another friend who moves into a new home in a new subdivision. Other friends who travel a lot or who have lots of adult toys like boats and 4 wheelers. We feel the need to keep up to them and dont want to admit we cant afford the luxury items.

Do you know someone like that?

So what do we do about it? One sure fire way to make sure we dont overextend ourselves financially is to use a “debt to income ratio calculator” Just a fancy term for a way to see if we can afford to buy certain things. There are several options to use for this but one I like is shown below. Its a simple process to use. Enter in your earnings. Be honest when listing your debts. Hit the calculate button. It will literally tell you if you can afford something else on top of your current debt load. Again, if you lie to the calculator it will lie to you lol. If you wanted a loan with a bank, anything over a 40% ratio and you will be out of luck.

But the best way to make sure you dont end up overextended is to be smart when making big purchases. Consider your current earnings. Do you currently have money left over from pay cheque to pay cheque? If you dont how can you afford more debt? If you have 500$ left over between you pay periods can you afford a new big payment? Financial problems can place massive pressures on your life including your relationship.

We would all like to think fiscal responsibility is a done deal but the reality it is its hard work and commitment to keep our head above water. Planning, self control and diligence when making purchases will keep you on the right path and reduce one of life’s great stresses.

In the immortal words of Samuel L!!

If you were wondering how big an issue this is check out how many memes are available. In this case I had no trouble finding all kinds of options to use in this post. While the reason for them is not funny it does indicate just how much trouble we are in. Just be aware, if you find yourself in this situation, you are not alone. In Canada, for every 1$ we make we owe 1.70$. How crazy is that as a country? And its reported to be worse in the USA.

So, if you find yourself in trouble but can’t seem to get out of it google this.”How to get out of financial troubles”. This will send you to a spot with multiple links to help you out. And if it doesn’t work modify the wording to better suit your needs.

For many people, we dont realize how important it is to be a good shopper. The difference in spending wisely and not paying attention to the cost of things can literally cost you thousands of dollars per year. While you may think that sounds ridiculous, picture this scenario.

You need groceries once per week. You spend 100$ on food one week then 150$ the following week when you need bigger items such as meat. There are 52 weeks in a year and it is very easy to save 10$ per trip to the grocery store(s) by selecting the store or stores where the pricing is best that week. The immediate effect is 52 weeks x 10$ is 520 dollars a year without working at it. And thats a conservative estimate for savings on your groceries

Now factor in your personal care items. Your big purchases. Your entertainment. Your clothing. The savings can be staggering.

There are many many web sites that describe how to become a better shopper. Below are some of the options but if you dont find something you like or is useful you should google more possibilities.

As a long time buyer I have developed some techniques to try and maximize my money when buying groceries. Have a read and see what you think. I am sure others out there have some other suggestions. Please feel free to send them in and I will get them posted.

Have an app on your phone or device for finding the best price on items that week. Simply search the app for what you really want and the bets price will be available to you. Apps such as flipp.com .. save.ca or redflagdeals.com can be invaluable

Learn the pricing. Likely the best way to save money when shopping is to know what the regular price of items usually is. Any company can list something is on sale but how do you know it actually is? Or by how much? If you have a good memory this is a simple task as you will quickly become very familiar with the cost of your normal purchases. If you have to, record them on your phone or take pictures of prices. Whatever works for you

Watch the sales tags. Companies will regularly put bright colored tags on items to indicate they are on sale. Make sure to read the tag closely. The fine print may not be what you expect it to be. The wording is key when looking at the tags.

Check your receipt. Always make sure to check your receipt after cashing out. Especially when there are sales items purchased. Sales prices are all supposed to be incorporated into a stores cash register and pricing system. The reality is there are many many times when items have been missed so you wont actually get the sale price listed on the store shelf. When you present this to the customer service desk you generally get it for free or you definitely get the sale price you were supposed to receive in the first place.

Look for the Slashed prices. In a lot of cases products that are nearing the end of their shelf life are put on sale.You will see the 50% tags attached to items like cheese and meats. You can save a fortune by taking advantage of this. Just remember to either use it quickly or package it properly and freeze it

Walk the aisles. This goes against normal thinking because experts will tell you the longer you are in the store the more you will spend. My belief is that by walking the aisles you will find deals you were not expecting. Sometimes it is an in store special. Or an end of the product line deal. or it could be a 2 day special separate form the normal weekly sales. If you have the time, take a look. But be disciplined!!

I didnt list using coupons as a great way to save money. The reality is thats a mistake on my part because any legal way that allows you to pay less at the counter should be taken advantage of.

I also didnt list shopping on line. I know its popular and can save money but I prefer to be there in person. Check out the veggies myself. Or find those special deals not listed in the usual way. Just my personal preference.

A couple of other things to think about … Eating healthy is expensive. You may have to decide how important it is for everything you buy. Buying name brand items can be overrated. Have a plan going into the store. And have patience 🙂

Our society today is very technologically advanced. We do so many things on line whether its banking, ordering food or buying goods. To make that happen, we generally need a credit card. They can be wonderful tools to have but can also create massive issues when not used correctly or respected properly. Below is a list of some of the main pros and cons about credit cards. I am sure there are others in both categories and it would be awesome if we had the opportunity to share them with everyone. So please if you know something important I have missed based on your own personal experience please message me and I will incorporate it into the post

Pros of credit card use:

1. Helps to build credit. It seems crazy but you have to use credit to actually build credit. If you buy everything with cash lending institutions have no idea if you are capable of making regular payments. Using a credit card and paying on it regularly produces good credit and the results can be better rates on house mortgages, car loans and other credit cards.

2. You dont have to carry cash. And if you lose the credit cards or have them stolen you get protection from the credit card companies with something called fraud protection. If reported immediately there will be little or no charge to you. Whichever bank/card you use make sure to read and understand the fine print out about fraud protection. KNOW YOUR RIGHTS!!

3. Track your spending. Have you ever noticed how easy it is to spend cash? I am a huge fan of using cash but it has its pitfalls. With credit cards it can actually be easier to stay on a budget. You can use your credit card statements or get updates on the balance There are apps you can use to track spending, provide budgets and generally give you a better idea of how you spend your money. The only way the apps work is if you have a record of your spending.

4. Earn rewards and perks. Many or most cards provide perks when using your credit card. You can build up points to be used for travel rewards and other such things. One of the big perks can be built in car insurance for renting a car. This can be expensive but many cards have this already installed as a feature. Again, know your rights with the card. Check out the link below to see which cards provide some of the best perks. Keep in mind the fees for maintaining these cards might not make it worth it.

Potential to overspend. Sometimes it seems too easy. Just pull out that card and swipe. But the reality is overspending is incredibly easy without some discipline from the cardholder. Once that happens you are then officially in debt. And getting out of credit card debt is one of the hardest things young people will ever do. There can be massive pressure applied to you internally when you fall into credit card debt. The interest rate makes it almost impossible to get ahead. Concerns about your balance and being able to use your card at all are a very real issue

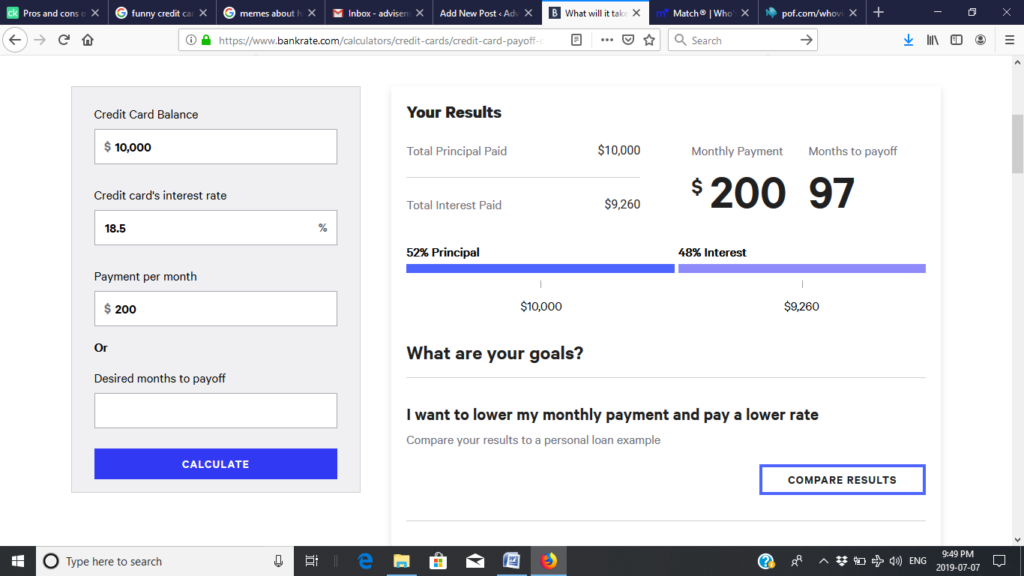

Below is an example of what 10,000$ in debt looks like when trying to pay it off

over 8 years to pay 10K at 200$ a month

Here is the link for the website so you can input your own numbers to see.

2. Fees and interest rates. With most credit cards you will be paying any annual fee for the card. The fees will usually be in the 120-150$ range but can be a little higher or lower depending. As for the interest rates, These can vary as well. Companies tend to offer low rates for s specified amount of time to get your business but the reality is you will be paying nearly 20% on any balance you carry from month to month. See below for some possible best rates available on cards.

3. Can negatively affect your credit score. Improper use of your credit card can have a serious affect on your credit score. If you have a low credit score this will seriously impede your chances of getting a mortgage/car loan/personal loan. The best way to minimize the effect is to make regular payments on time. But just know that if you are carrying a high balance in relation to your available credit your ability to borrow money will be affected. See below for a description of what a credit score is in Canada.

So those are the pros and cons as stated by various sources. Please feel free to search other sites for yourself to see what others have to say about the pluses and minuses of owning and using credit cards.

Like most things in life, there are pros and cons to using credit

cards. If you’re smart about how and when you use your plastic, a credit

card can prove to be an essential and useful financial tool.

If you allow your spending to get ahead of you and you’re not

organized when managing payments and accounts, credit cards may do more

harm than good.

If and when you decide to apply for a credit card, make sure you pick the one that’s the best option for you

And now my personal opinion. Since I was like 15 years old I had a credit card. My first card was linked to my fathers account. I learned the hard way about not making payments an unfortunately it fell on my dad to bail me out a couple of times because I was too busy spending other money I didnt have to make the necessary payments. It was embarrassing and humbling to say the least. And making basic payments will never let you catch up

In the ensuing years I have used the cards much more wisely. I better understand the ramifications of pulling out the plastic and I do it now when it is required. They have granted me all sorts of bonuses and perks including booking hotels and rental cars using points I have built up. I havent always done a great job of paying them off monthly but its far better than it ever was. And paying the bill off every month is literally the only way they work for you. Keep it in mind and spend wisely.

I have also had my credit card information stolen. Its simple when you travel abroad. You are required to supply a credit card to any hotel you stay in. Just keep in mind that any card reader can extract your information and copy the card. From there the clever a-holes out there can use your card to make purchases before the card can be cancelled. Its one of the main reasons informing your credit card company if your impending travel. they would then recognize if unwanted purchases are being made

Also remember to switch cards as and when required. Dont stay with a certain card “because I always have or thats who my parents use”. You will generally get better rates when starting with a new company and it can be a good way to help you catch up. And just remember when people tell you to maintain a balance on your credit card to help improve your credit rating a balance can be 1$ or a 1000$ and the effect is the same.

As previously mentioned I am hoping any readers out there will share their own views on credit cards. It can be a contentious subject to say the least but talking about it will always make us better informed in the long run

Nowadays many kids receive money for special occasions rather than presents. This could be for Christmas or Easter. Birthdays or grading day in school. Whatever the reason kids tend to have a lot more cash floating around than we ever did growing up.

So what do you do about that? The smart thing is to put it into the bank. You dont have to put all of it into the bank but it makes sense to bank some rather than keep a bunch of bills lying around. Its always at risk of being lost or borrowed or more likely that you tend to spend more when you see lots of cash right in front of you.

So how do you go about putting it into the bank? For adults its a simple thing now to go online to a bank’s website and open an account in a few minutes. But what about for younger people? There are some rules you need to follow but its a pretty simple process. The bottom line is you cant open your own bank account until you turn 18. Until then your parent or guardian must co-own it with you.

Follow the link and let WIKI tell you how. https://www.wikihow.com/Open-a-Bank-Account

And keep in mind there can be charges related to your new bank account. The good thing about being your age and likely a student is that banks don’t charge any kind of service fees. Check out the links below to see how you manage the new account and what you get with the type you choose. https://www.td.com/ca/en/personal-banking/products/bank-accounts/chequing-accounts/student-chequing-account/

And there you have it. A simple process to have a place to easily put your money. It keeps it safe and secure and you can watch it grow as you continue to add to it. The reality is there is nothing earned (or very little) in interest on your money. Banks will usually offer you a higher rate to sign on with them but there is generally a time limit on that rate and it will then settle somewhere between 1 and 2%

One of the scariest things you will do as a young person is attempt to find a job and enter the work force. We all have an innate fear of rejection that makes this process almost overwhelming at times. In some cases the NEED for a job increases the pressure we are feeling. Below is a general guide you can use to prepare yourself for the job search.

Decide on what you would like to do. But be realistic about it. Understand that without education or training your options are going to be limited. Looking on job sites can help you to understand which companies are willing to hire you without any experience. Some of the best places to apply are Tim Hortons and McDonalds (excellent training program). They may not be the glamorous jobs you envision in your future but they do provide an excellent start. Don’t be ashamed of finding your first job … or your second

2. Write a resume for yourself. This is an extremely important part of the process. It is your one chance to provide a potential employer with a reason to hire you over the other applicants. The trick is it can’t be too long or too short. Employers are looking for a couple of key things and don’t want to be bogged down with too many details. A few excellent sites showing what to include in your resume are listed below.

3. Work on your appearance. I know you all like to have your own sense of style. For some it’s a lot of piercings and for others it’s a lot of ink or tats. Or different coloured socks. The problem is it may not be what employers are looking for so you need to be ready to adapt how you look to suit where you’re going to apply. For instance, if you apply to mow lawns you can likely be a little more liberal with your appearance than if you apply to work in a bank. And so on. Asking your parents or teachers might be a good place to go for advice on this.

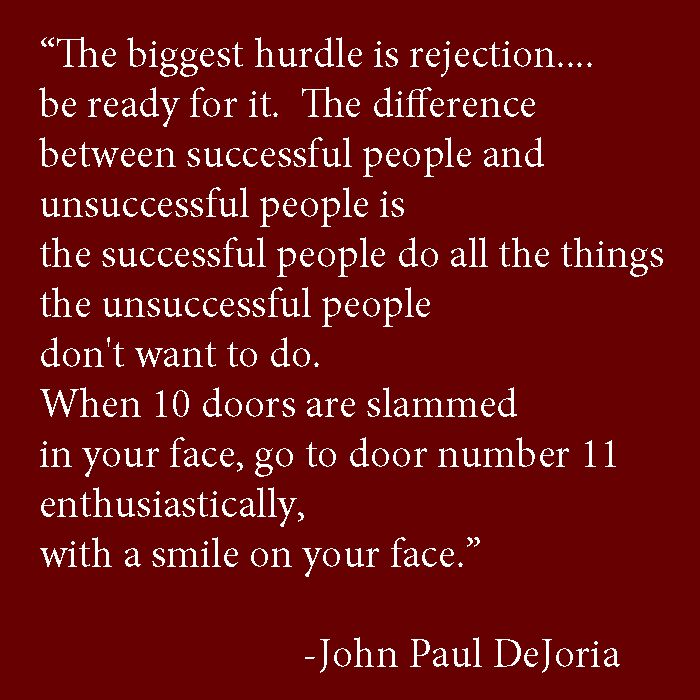

4. You need to prepare yourself mentally for the big “NO” when applying for jobs. The reality is there could be many applicants for only 1 or 2 spots. And its very possible the manager doing the hiring has certain things in mind they are looking for. You cant get disheartened if this happens to you. I can pretty much guarantee you will be turned down at some point in your professional career. Don’t let that define you. Tell the business owner or manager you appreciated their time and that if there was a chance in the future you would hope to be considered. Simply walking away indicates you were never really serious about the job.

If you don’t know who JP DeJoria is then google him. Pretty cool story.

Check out the link below to see how some rather famous people have done after being rejected. Not sure I would do what Madonna did but I bet it was funny to be there

5. At the risk of sounding like a parent, this list wouldn’t be complete without adding this item. You absolutely need to stand up and be mature when meeting with a potential employer. How you carry yourself is critical to showing the employer you are serious about the application. Keep your head up. Maintain eye contact as much as possible. Have a firm handshake. Be as confident as you can even if you don’t feel like it. And lose the electronics. Its a deal breaker for almost all places. Simply turn them off.

6. Last item is to do a follow up. For some it is considered the most important part of getting a job but the reality is its just one more part of the process. For employers it shows you have a real interest in the job and sets you apart from many of the others. It can be an excellent way to have them take a second look at your resume. Wait about a week (less if you know the hiring timeline) and place a call to the employer. Its vital you speak to the person doing the hiring so don’t leave a message with someone and hope it gets passed on.

There are

no guarantees but if you can follow those 6 steps you will improve your chances

of being hired. There are certainly other things you can do but the idea is to

give you the basics to start with and you can adjust to what works best for

you. As part of my work experience I have performed interviews with potential

candidates. Here are a couple of things to keep in mind.

At some point make sure you tell the employer you really want the job ( provided you actually do). They love to hear you’re interested in the position. Trying to act cool and casual doesn’t cut it. DON’T EVER tell them you need the job. That gives them wayyyyy too much power over you.

Be early for the interview if possible. 10 -15 minutes is a good guideline. If you can do a little research on the company you are applying to. It is very common for a manager to ask “what do you know about us”. Always good to have an answer to that.

Speak clearly and concisely with the best

grammar you are able to. Make sure you look the person or people in the eye

when you speak to them. Don’t be afraid to take a moment to form your thoughts

before replying to a question. Better to get it right the first time

Lastly … at the end of the interview, if they

have time, ask them how they thought the interview went and what could have

been improved. It may not help you with that particular job but it will better

prepare you for future interviews. You may also find out you forgot to provide

them some information about yourself that could change the final outcome. Don’t

be scared to ask.

It has taken me 2 years to get the gumption up to start this blog. I am very opinionated so I try to let people live their own lives and learn as I did … usually the hard way. It helps me to avoid annoying more people than necessary. But not so long ago I was in a conversation with some younger people. The topic doesn’t really matter but it again proved to me this blog might be a good idea .

You see during the conversation I realized again how so many young people simply haven’t been given the information or skills required to make certain choices and decisions. In many cases they don’t even realize they should know about certain things. Having 2 kids of my own, I have been involved in such discussions before either with them alone or in the presence of their friends. For whatever reason this conversation provided me with the impetus to get this started. I suppose it was simply time.

So here I am …. About to embark on a journey to share some hard earned

information to those out there willing to take a few minutes and read this in

hopes of making their lives a little easier. To be honest most of this should

be bundled into a school program to help kids navigate through the pile of crap

they face on daily basis. Currently that isnt the case so I will do my best to

share some things I have learned over the years. I cant guarantee you I will

always be right. Or that you will always agree with what I say – of that I am

sure. But I promise I will do my very best to give you the best, most current

information out there.